Inflation risk in the construction materials market: It ain’t over yet!

By David Bowcott

Risk Management

David Bowcott

There is no doubt that the pandemic has done a number on the supply chain in the construction industry. Last year was filled with dramatic price increases that hit many of the materials used in building projects of all sizes and scopes. The bad news is that the uncertainty is not over just yet, but there are steps you can take to help navigate this uncertain future.

Most prognosticators felt the upward movement on pricing would be temporary as the economy repaired the disconnections within the supply chain that were created or strained by COVID-19. As the pricing increase fervour heated up, it appeared to peak in early summer of 2021, leading some to believe the worst of the inflationary pressure within the construction sector was over as summer came to a close.

As the price for lumber dropped from its June 2021 high by as much as 62 per cent, many predicted an end to the steep construction material price increases.

Was this the beginning of the end for inflation within the construction materials economy? Nope. It seemed that prices for many of the other construction commodities continued to rise, despite lumber’s reversal.

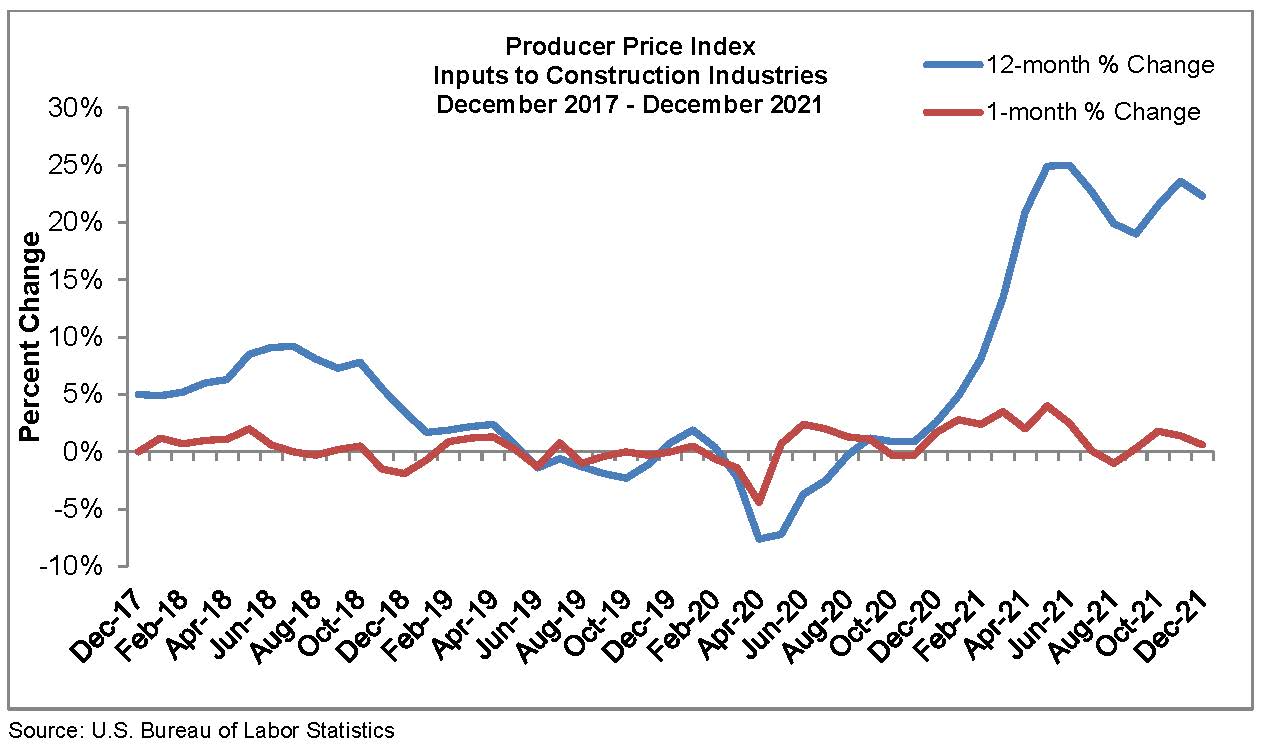

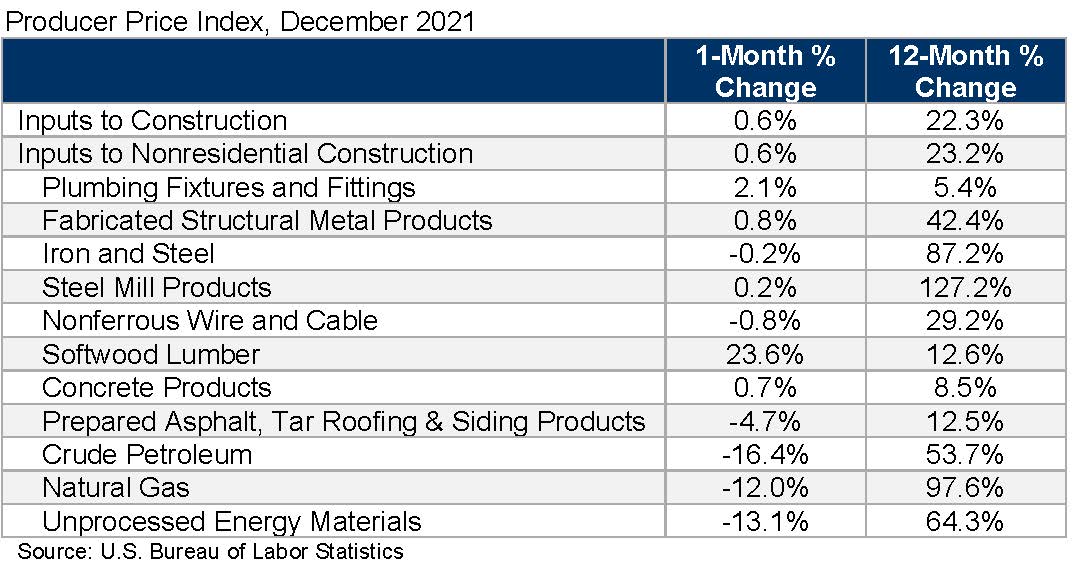

(Source: Associated Builders and Contractors)

Pricing for steel, wire, nails, gypsum, asphalt, mechanical systems, fixtures and many other products continued to climb as the construction industry approached the end of 2021. Information shared by Associated Builders and Contractors in the U.S. illustrates the trend of rising prices for many of the major construction materials categories.

(Source: Associated Builders and Contractors)

Many of these upward pricing trends in construction commodities, referenced in these graphs, don’t appear to be reversing and, what’s worse, is that we are seeing lumber prices creeping up once again as of November-December 2021.

Many factors related to the pandemic are creating this disconnection between demand and supply within the global construction marketplace. The following are but a few underlying causes for the inflationary pressure in the construction inputs sector:

- Reliance on a “just-in-time delivery” model within our global supply chain.

- Centralization of our supply chain in countries with low labour costs.

- Loss of domestic manufacturing capacity over the past several decades.

- A highly fragmented supply chain (one chip from Taiwan can leave you with a non-functioning mechanical system).

- COVID-19 workplace shutdowns.

- Cross border requirements under the COVID-19 economy.

- The impact of “the great resignation” on the supply chain and logistics industry (trucking has a staffing crisis).

- The growing demand for material goods as consumers suddenly have more funds available for building projects since vacation plans, and expenses, were set aside.

To add gasoline to the fire, we are in the midst of the fourth wave of COVID- 19 as the Omicron variant rips through the global economy at a rate previously unseen. Though it appears this variant isn’t as severe as previous strains of the virus, it is still causing varying shutdowns in parts of the global construction supply chain. This wave will no doubt exacerbate many of the above root causes, creating further inflationary pressure on construction material supplies.

As this inflationary cycle doesn’t seem to be ending any time soon, it is prudent to consider steps your organization can take to minimize risk.

Here are a few suggestions that may be helpful to managing this risk on current and future projects:

- Consider qualifying your bids to ensure your subcontracts align with your prime contract.

- Educate your customers about the supply chain disruptions as this disruption is widely known at this point and it could be considered an event which allows you to share risk with other parties to the contract.

- Use technology to better track supply chain disruptions. Several technologies are in the market that can give you advance warning of supply chain disruptions.

- Use supply chain risk finance solutions, such as subcontractor default insurance, supply chain insurance, and input price insurance. Input price insurance is a new product in the market that simplifies commodity price hedging and brings many benefits to the hedging process that could not be realized via derivatives hedging.

- Press governments for support and encourage them to create a more resilient supply chain by enacting legislation that would grow domestic manufacturing capacity.

- Consider sourcing supplies not solely on lowest price. Consider the reliability of getting supplies delivered on-time.

The above suggestions are but a few that could help your organization deal with this risk that doesn’t appear to be going away any time soon — despite what the prognosticators are saying.

David Bowcott is Global Director – Growth, Innovation & Insight, Global Construction and Infrastructure Group at Aon Risk Solutions. Please send comments to editor@on-sitemag.com.